Does Insurance Cover Therapy? How to Calculate Your Cost

Get a clear estimate so you can start therapy with confidence.

Let’s face facts: Calculating the cost of therapy can be a real headache.

If you’re already struggling with your mental health, the last thing you need is another obstacle to getting help. With insurance being so challenging to decipher, it can be discouraging to try to access your benefits.

If you’ve avoided mental health care up until now, you’re not alone. Mental Health America reports that from 2019-2020, 42% of adults with mental health conditions did not receive treatment because of the cost, despite the fact that most have access to insurance (compared to the 10.8% who do not).

Among those who are able to receive care, many are paying hundreds of dollars out of pocket each month to see a therapist. No doubt, the arduous process of navigating insurance has become a huge deterrent in accessing affordable care.

The good news is, thanks to federal and state parity laws, your copay (the fee you pay per session) for therapy is unlikely to be much higher than it would be for any other medical doctor. Which means affordable mental health therapy may, in fact, be within reach.

Read on for our best tips to calculate the cost of therapy.

Know your policy

To start, you’ll want to review your insurance policy — more specifically, your EOB (Explanation of Benefits). You should have received this when you enrolled, but you can always request a new copy from your insurer.

Under your EOB, the cost of mental health services should be listed, including therapy, under “allowed amount.”

If your therapist’s fee is $125, for example, and your copay is $50, you would pay $50 for each session. Insurance would pay the remaining $75.

Copays only apply to therapists who are “in-network.” This means they have a predetermined agreement with your insurer to be part of their network of providers and therefore can take your insurance.

Therapists who are “out-of-network” do not take your insurance, so the copay would not apply. You’d have to pay the full amount they charge, regardless of what insurance policy you have. You may be eligible for reimbursement with out-of-network benefits. Be sure to check with your insurer to see if you qualify.

Also, familiarize yourself with whether or not you have a deductible to reach — this is the amount you’ll pay out of pocket before your insurance kicks in.

If you haven’t met your deductible yet, you will have to pay the full cost of therapy until it’s been met. If you’re looking to make therapy more affordable in the meantime, you might space out your sessions. For example, you could go every other week instead of weekly.

Remember that any medical services can count towards your deductible, not just therapy.

Calculate the cost of therapy

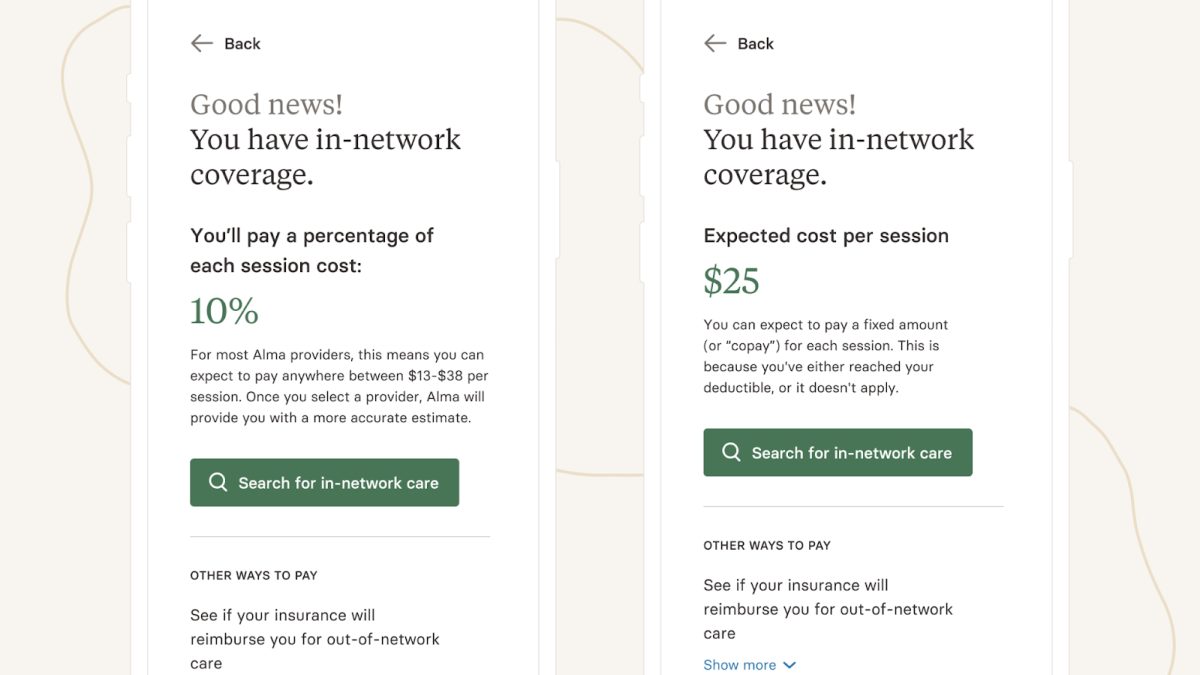

If your EOB isn’t accessible to you or you’d like to save some time, Alma provides a free Cost Estimator Tool. This tool can quickly calculate the cost of your copay, as well as letting you know how close you are to meeting your deductible.

All you need is your name, date of birth, insurance provider, and member ID (your information is secure and will never be shared!). You can leave the rest to us!

Reach out to your insurer

You may find that you have additional questions about your insurance policy. We recommend reaching out to Member Services (the number is usually located on the back of your insurance card or online), or, if you receive your benefits through your employer, your HR department may be able to help.

Mental Health America has a great list of questions to ask your insurer. Some of these questions include:

- Do I need a referral from my primary care physician to see a mental health professional?

- Do I need any pre-approval from the insurance company before I see a mental health professional?

- Do I need to see someone “in-network” (part of a list provided by your insurer) or am I free to choose any qualified professional?

- What will I be charged if I see an in-network provider versus an out-of-network provider?

- Are there limits on how many sessions will be covered by insurance?

- Is there a specific list of diagnoses that are covered?

Take action:

Don’t let the cost of therapy stand in your way.

If you’ve struggled in the past to find a therapist, Alma’s free directory can connect you with providers who take your insurance and have availability for new clients. Our clients have access to a diverse network of over 10,000 providers in the United States, saving an average of 77% on their cost per session.

Related Articles

Nov 21, 2022

Looking for a therapist?

Get tips on finding a therapist who gets you.

By subscribing to emails from Alma, you are agreeing to Alma's privacy policy.